House of Cards: China's Market Crash

(Source: Bloomberg.com)

Written by Dae-Han Song (chief editor, World Current Report)

After peaking on June 12, 2015, the Shanghai Composite Index plummeted, wiping out $3 trillion. While such loss may appear staggering, the size of China’s stock exchange is only 30% the size of its real economy.[ref]Developed countries have financial markets that are larger than their real economies.[/ref] No more than 3.7% of its households invested in the stock market, and they invested less than 15% of their household assets. While much of the speculative investment was made with bank loans, the loans constituted just 1.5% of total bank lending in China. Thus, it didn’t take long for the market to stabilize by September. Now, it is back to its pre-bubble levels, still higher than last year. Yet, the market crash is but the tip of a much larger underlying problem: overinvestment during economic stagnation and investment that produce high returns but pay little to workers and to those that save (and hence lend).[/p]

Since the 1990s, China’s economy has been driven by export oriented production in the coastal areas. To make them globally competitive, China provided these companies low-interest rate loans and suppressed worker wages[ref]China suppressed workers wages through its household registration system that denies welfare services to migrant workers, thus making it easier to exploit them for lower wages. This in turn puts a downward pressure on other worker’s wages. Migrant workers make up more than a third of workers.[/ref] while maintaining a cheap currency and lax regulations. These engines of export-based production led to China’s tremendous GDP growth and trade surplus. However, in the aftermath of the US financial crisis, the global economic slowdown has meant less demand for China’s exports. To counter slowing demand for its exports, and to stave off social instability,[ref]China needs at least 7% GDP growth for social stability. Given an unequal political and economic structure, a certain percentage of GDP growth would be required for social stability. Only a sufficiently high flow of GDP growth can guarantee that after profits are soaked by the top tier of society, enough may trickle down to satisfy the needs and expectations of the many at the bottom. In 2000, He Qinglian divided Chinese class structure into the elite at 1% of the population; the middle class at 15%; workers, rural-urban migrants, and peasants as 69%; and the unemployed and rural poor at 14%. China’s Listing Social Structure[/ref] China carried out an immediate stimulus package focusing on fixed investments mostly cheap loans.

Yet, increasing investment (as a share of GDP) amidst a slowing economy will result in excess capacity. State owned enterprises (SOEs) took on so much of this debt that in the context of a slowing global economy it had little chance of producing profit. Solving this problem involved decreasing the debt on SOEs, and increasing domestic demand to absorb excess capacity. The government’s solution was a stock market bubble that could create wealth among the population and increase domestic demand, while paying off its debt by selling a portion of SOE’s equity (albeit a non-controlling portion[ref] The government controls either a majority of shares or a large minority to prevent shareholders from controlling the company. Thus, while an SOEs stocks are privatized the state still retains control of management.[/ref]).

Investors, mostly individuals, were more than willing to rally around the government’s loose credit policies and exhortations to buy; the increasing risks tempered by the belief that the government would bail them out. However, underlying the desire to participate in the stock market was another underlying contradiction in China’s economic model: low wages and interest versus high profits. Despite the high returns on investment, people are paid low wages for their work and low interest on their savings. When cheap credit was provided to reap the benefits of high profits, people rationally rushed into the stock market.

Why did the government gamble on a financial bubble to absorb excess production and solve its debt problem rather than implement policies to boost domestic demand? While boosting domestic demand is the rational choice, the government chose the stock market bubble because doing the former would require a redistribution of income that would undermine the short-term interests of the elite: It would require a reversal of policies prioritizing profits for companies at the expense of low wages for workers. Who can bring about this rational choice not simply for workers but for social stability?

Despite its 40 years of reckless and destructive pursuit of growth, the Chinese Communist Party clings to its revolutionary identity. Yet, on its own, it appears unable to turn from the marketization[ref] The Chinese Communist Party is not monolithic. It can be divided into two equally powerful factions: the Elitists and the Populists. The Elitists includes the “princelings” (children of high ranking officials) and is more focused on rapid GDP growth. The Populists include those that rose through the Chinese Communist Youth League and are more focused on social cohesion. Hu Jintao is part of the Populists and during his presidency he focused on creating a “harmonious society.”[1] In his last three years in office, he managed to stabilize inequality.[2] [1] Hu Jintao’s Road Map to China’s Future [2] What Did Hu Jintao and Wen Jiabao Do For China?[/ref] it has driven forward since 1978 and from which its top members have profited.[ref]He Qinglian describes the political and economic elite as those that have either extracted rents from their positions of power during China’s marketization or family members who have benefited from such connections. China’s Listing Social Structure [/ref] In response to the negative impacts of its policies, currents within the party emerged to carry the banner of social justice and equality. In 1993, after Deng Xiaoping’s calls for more rapid marketization led to a restructuring of state enterprises and the lay off of 3 million state workers,[ref]Between 1993 and the end of 2002, 44% of jobs in the SOEs were eliminated. A Chinese Alternative? Interpreting the Chinese New Left Politically [/ref] a “New Left” emerged to advocate for China’s shift from marketization and towards greater equality and social justice through state intervention. Yet, unwilling to put forth a clear program in advance, it awaits the rise of social movements.[ref] As Wang Hui, one of the leading intellectuals of the New Left states, “When social movements do emerge, we should study very closely what sorts of reasons bring ordinary people into them.” Fire at the Castle [/ref].

Such a movement will come from China’s workers. Since the marketization of the economy, there has been a rapid increase in the share of nonagricultural workers (mostly wage workers) from 31% in 1980 to 50% in 2000 to 60% in 2008 making them a powerful force in society. At the same time, demographics is on their side as those aged 20-59 will decline from 853.7 million in 2015 to 781.8 million by 2030, 743 million by 2040, and 650.9 million in 2050.

In addition, more and more migrant workers (about a third of the workforce and the most economically vulnerable) are opting out of migrating to coastal areas for work instead choosing to work inland near their homes. A large number of these migrant workers are part of the “second generation” of migrant workers born after 1980 who have higher expectations and demand better working and living conditions.

graph2

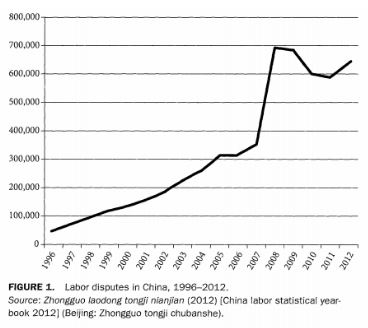

Graph 1: The curve displays the growing number of labor disputes in China between 1996 and 2012 (Source: Insurgency Trap: Labor Politics in Postsocialist China)

These factors strengthen the position of workers’ in society in their struggles. As inequality deepens, workers struggles multiply exponentially. As the graph above shows, labor disputes have steadily increased by the hundreds of thousands. However, they have not yet come together into a social movement demanding systemic change. That is because most of the strikes are fights over unpaid wages that happen autonomously outside the government sponsored unions. Without a democratic union to voice their demands, many of these struggles remain isolated and do not translate into demands for broader systemic change. This inability to institutionalize insurgency results in an insurgency trap where workers struggles cannot come together to change their politico-economic reality through systemic change, and the government is unable to diffuse the “insurgency.”

To achieve greater harmony in society, the Chinese Communist Party must give workers a way to change society. They may be the only ones capable of shifting China’s development towards rational, sustainable growth based on social justice and equality.

Given China’s vast population, economy, and central position in global production, a victory for workers in China would reverberate across the global capitalist commodity chain.